The great termination? More organizations are terminating payer contracts amid heated negotiations, and Medicare Advantage is in the hot seat.

The payer/provider battle is raging, and signaling what may be an emerging trend: More organizations are fighting back against payers by terminating their contracts completely, and Medicare Advantage (MA) has seemingly been the focus.

Thanks to record inflation and operational challenges, hospital and health systems find themselves with their backs against the wall in negotiations, leading CFOs to initiate contract terminations.

But what exactly has led to the turmoil? CFOs say the reasons are vast.

“Bad behavior.”

More organizations are now considering contract terminations due to dissatisfaction with reimbursement rates and overall bad payer behavior.

Healthcare providers have been arguing for years that insurance payers often set reimbursement rates at levels that are lower than the actual cost of providing care. Couple this with skyrocketing inflation costs and labor expenses, and providers can be left with no other choice.

When reimbursement rates are significantly lower than the cost of care and the administrative burdens are so high, healthcare providers may experience unsustainable financial losses. These underpayments along with egregious denials are pushing providers to the limit.

In such cases, CFOs may weigh the option of contract termination as a last resort to protect the financial stability of the organization.

“There is rarely one final straw, but rather, a cumulation of events that negatively impact the fiscal viability of the relationship,” Britt Berrett, managing director and teaching professor at Brigham Young University and former CEO with HCA, Texas Health Resources, and SHARP Healthcare, explained.

“Long before rates become contentious, hospitals are dealing with bad behavior and payer shenanigans,” Berrett said.

For example, he says, payers are rejecting claims based on utilization review criteria. Many healthcare leaders consider these rejections to have little to do with utilization but rather an attempt to refuse payment.

Luckily for providers, organizations are becoming more capable of cost accounting and utilizing analytics to determine the actual cost by patient and payer.

Why Medicare Advantage?

Why has MA been in the hot seat of terminations? While not the only culprit of the turmoil, organizations have been fighting back against MA’s low reimbursement rates for years, and as Berrett said, maybe CFOs are finding no fiscal viability in the relationship with the payer.

One case in point is Scripps Health. Two medical groups within the system canceled their MA contracts for 2024 because of low reimbursement rates, denials, and administrative costs to manage high utilization and out of network care.

“We’re unfortunately on the vanguard of what I think is going to be a very ugly few years between hospitals and commercial insurance companies,” Chris Van Gorder, president and CEO of Scripps, told USA Today.

And Scripps has the resources to better manage these burdens, meaning these burdens are even more exacerbated for smaller systems.

An example of this is Samaritan Health Services. It recently terminated its commercial and MA contracts with UnitedHealthcare.

The five-hospital, nonprofit health system cited slow processing of requests and claims that have made it difficult to provide appropriate care to UnitedHealth's members, according to a news release from Samaritan.

“This, along with other factors, is not in alignment with our mission of building healthier communities together,” the health system said.

Another example is St. Charles Health System, a four-hospital network and healthcare company in Central Oregon, which terminated its MA contracts in 2023.

Steve Gordon, president and CEO of St. Charles, said great thought went into the decision to reevaluate MA participation, and it was done only after years of concerns piled up not just at St. Charles, but at health systems throughout the country.

“The reality of Medicare Advantage in central Oregon is that it just hasn’t lived up to the promise,” he said in a press release. “A program intended to promote seamless and higher quality care has instead become a fragmented patchwork of administrative delays, denials, and frustrations. The sicker you are, the more hurdles you and your care teams face. Our insurance partners need to do better, especially when nurses, physicians and other caregivers are reporting high levels of burnout and job dissatisfaction.”

It's also worth noting that Memorial Hermann Health System, the largest hospital system in the Houston region, terminated its agreement with Humana's MA networks at the beginning of the new year. Memorial Hermann has not yet publicly cited why, other than saying the contract negotiations hit an impasse.

OK, but what’s the outcome of termination?

But what is it like on the other side of an MA termination? It hasn’t been so bad for some.

Hamilton Health Care System, a not-for-profit, fully integrated system of care serving the northwest Georgia region, has been out of network with MA for years.

“We are not currently in network with any Medicare Advantage plans. We would end up netting less than traditional Medicare because of denials and administrative hassles,” said Julie Soekoro, EVP and CFO at Hamilton Health Care System.

In addition to a lessened administrative burden, being out of network hasn’t affected Hamilton’s bottom line or patient experience.

“Since we are out of network, the MA plan should be paying us as if the patient were a regular Medicare patient, so it has not affected the patients adversely,” Soekoro said.

All the time and money spent on takebacks, pre-authorizations, and denials add up. Coupled with the aforementioned low reimbursement rates, CFOs can find it doesn’t make business sense to continue with the payer.

MA isn’t the only difficult payer, though; the challenge is universal.

For example, Hamilton Health Care has spent a lot of time going back and forth on a contract with a national payer that wanted to bring them in network, only for Hamilton to walk away from the negotiation table.

“After spending a great deal of time and effort modeling the contract, we learned the payer will require all diagnostic imaging business to go to a freestanding competitor, while building in very attractive looking rates for imaging,” Soekoro said. “This is misleading in that they never intended to allow their subscribers to come to us for imaging.”

“This was discovered incidentally by our contracting director, rather than fully disclosed by the payer,” she added. “Also, certain provider-favorable terms that we built into the language have mysteriously fallen out of the most recent version of the language.”

As stated, Hamilton walked away from that particular negotiation.

Another example comes from Berrett and his time at Texas Health Resources.

While Berrett didn’t specify the type of plan (MA or otherwise), the organization terminated a payer contract because its patients had significantly higher CMI, resulting in losses for their patients.

“The impact [of terminating the contract] was very positive for the hospital. We lost volume but improved margins,” he said. “The payer was able to promote a significantly lower premium for companies because their rates to the providers were so low. When we terminated the agreement, they could no longer sell lower premiums and their market share dwindled. They eventually retreated from the market.”

What does the future hold?

It’s worth noting that the trend of MA terminations is not a common occurrence with the nation's health systems—yet. In fact, several health systems expanded their own 2024 MA subsidiaries.

But that hasn’t stopped the critiques of the program from growing louder.

The Health and Human Services Department’s inspector general reported last year that some MA plans have denied coverage for care that should have been provided under Medicare's rules. On top of this, CMS and the Biden Administration have both proposed rules to address certain aspects of the plan’s requirements.

Even so, the payer/provider relationship is sure to remain heated in the coming year—even beyond MA.

“At the same time that community hospitals are struggling to stay out of the red, the national payers are reporting profits in the billions in their quarterly earnings reports,” Soekoro said.

“It feels to me like the payers became accustomed to taking in premiums during the volume downturns of the COVID years when patients shied away from seeking follow through on regular—and sometimes even urgent—healthcare needs,” she said. “Now the payers seem to be looking for ways to sustain those increased quarterly earnings.”

As for the providers, CFOs could have more leverage in negotiation talks than they think, but it requires willingness and preparation to pull levers that may be uncomfortable yet necessary for financial survival.

Dropping a payer is “absolutely an important strategy,” Berrett says. “Providers are becoming more capable in measuring the impact of the slow or rejected payments, and providers are looking at the actual cost of care by patient. Payers need to be aware that.”

There are two important considerations for providers, Berrett says.

“Are we able to collect our negotiated rates, and are the patients covered by this payer more expensive to treat?”

This year won't be easy for CFOs, but there are a few ways to set an organization up for success.

Stimulus funds are gone, median revenue growth is still slow, and expenses are continuing to increase due to a reliance on expensive external contract labor and increased wage costs.

Luckily there are many ways hospital and health system CFOs can make sure they are setting their organization up for success, and Brett Tande, CFO of Scripps Health, recently shared four of them with HealthLeaders:

It’s clear that labor challenges—and the cost of that labor—will continue to be a prominent concern for healthcare organizations. As a handful of various industries have participated in massive strikes in 2023, the trend in healthcare is likely to continue.

That being said, hospital CEOs and CFOs should anticipate—and prepare—for some heightened labor negotiations this year.

The Kaiser union’s disagreement over across-the-board raises in 2023 was a significant financial concern, however, not uncommon. Hospital leaders must carefully assess the impact of wage increases on their budgets, especially when facing demands for higher pay. Balancing fair compensation for healthcare workers with financial sustainability is going to have to be top priority.

Bringing down labor costs is an area of focus for many hospital CFOs, but not at the risk of creating staffing turnover. Cost savings can be undercut by the resources required to replace workers, including interviewing candidates and training new employees.

New workers are also less productive in their initial transition period than established staff, which leads to less revenue. These factors should be considered when hospital leaders weigh the threat of losing workers by not meeting wage demands.

Wage laws

Even if your staff is happy, that doesn’t mean you won’t be required by law to increase wages across the board.

Take California for example.

California Governor Gavin Newsom signed a new law that will gradually raise healthcare workers' hourly minimum wage to $25, a bill that has an estimated price tag of $4 billion for the 2024-25 fiscal year.

But, that estimated $4 billion price tag is just at the state level and doesn't necessarily include the costs for private organizations or those in the non-profit healthcare world, so CFOs in California in particular really need to strategize for this unknown added cost.

As for CFOs outside of California, while wage increases weren’t as high as California, many states saw a wage increase on January 1.

What more can CFOs do?

Organizations need to recruit and retain talent in house and on a budget.

Gone are the days when CFOs of smaller (and even large) organizations can throw money at the problem—i.e., salary increases and bonuses—to attract and keep talent, especially when a hospital 20 minutes down the road can pay their staff much more for the same job.

So, what can leaders do to bolster the workforce while keeping expenses low? Placing an emphasis on culture and scheduling flexibility is a great place to start.

Here are several budget-friendly strategies that I have complied from talks with CFOs across the country that other leaders can employ in 2024:

Asses your employee benefits and perks: Offer a comprehensive benefits package that includes health insurance, retirement plans, and additional perks such as flexible work schedules, wellness programs, or tuition reimbursement.

Prioritize training and staff development: Provide budget-neutral ongoing training and professional development programs. Staff value opportunities to enhance their skills and advance their careers, so offering educational support, workshops, or mentorship programs can demonstrate your commitment to their growth. Cross-training employees in various roles within the organization is also a great way to enhance schedule flexibility and help bridge staffing gaps.

Form recognition or reward programs: Implement a robust recognition and rewards program to acknowledge and celebrate employee achievements. Non-monetary rewards, like public recognition, awards, or personalized thank-you notes, can boost morale and motivation.

Emphasize work-life balance: Promote work-life balance by offering flexible scheduling, remote work options (where feasible), and paid time off. Emphasizing the importance of a healthy work-life balance can help attract and retain staff.

Implementing wellness initiatives to support employee health and reduce burnout can also help in this area too. These programs can include stress reduction workshops, access to fitness facilities, and mental health support.

Create career advancement opportunities: Create a clear career path within the organization. Staff are more likely to stay when they see opportunities for advancement. Encourage internal promotions and provide training for leadership roles.

Streamline existing technology: Be creative in ways to bolster the technology and tools you already have to streamline workflows and reduce administrative burdens. This can improve staff efficiency and allow them to focus more on patient care.

Prioritize community involvement: The attendees agreed that many healthcare professionals—especially those in more rural areas—are motivated by a sense of purpose and making a difference in the community, so highlight your hospital's role within the community and engage employees in community service or outreach programs.

Incorporating a combination of these strategies can help small and medium-sized hospitals strengthen their workforce, improve staff satisfaction, and remain competitive in the healthcare industry without solely relying on salary increases.

In a field of 2,644 short-term, acute care non-federal US hospitals, Forbes says there were 100 organizations—which represent teaching and community hospitals of various sizes—that stood apart and serve as guides for the broader industry.

This list measured patient outcomes and experience, operational efficiency, financial health, and community impact, to see which organizations came out on top. And according to PINC AI’s analysis, there’s much to gain in following their lead.

“If all hospitals performed at the same level as the 100 Top Hospitals, more than 272,000 additional lives would be saved in the hospital and more than 432,000 additional patients would be spared complications as a result of care. $15.7 billion in inpatients costs would be avoided,” the report says.

While the entire list is available in the report, let’s take a look at the top 10 major teaching hospitals and large community hospitals:

Top Major Teaching Hospitals:

1. Baylor Scott & White Medical Center - Temple

Location: Temple, Texas Clinical outcomes:★★★★★ Operation efficiency: ★★★★★ Patient experience:★★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 13 Website

2. Trinity Health Ann Arbor Hospital

Location: Ypsilanti, Mich. Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★★ Financial health: ★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 13 Website

2. Baylor University Medical Center

Location: Dallas Clinical outcomes: ★★★★★ Operation efficiency: ★★★★ Patient experience: ★★★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 5 Website

4. St. Luke's University Hospital - Bethlehem

Location: Bethlehem, Penn. Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 11 Website

5. University of Utah Hospital

Location: Salt Lake City Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★★ Financial health: ★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 6 Website

6. NYU Langone Health - Tisch Hospital

Location: New York City Clinical outcomes: ★★★★★ Operation efficiency: ★★ Patient experience: ★★★ Financial health: ★★★★ Community health survey performance: No survey data Total number of years on 100 Top list: 2 Website

7. Vanderbilt University Medical Center

Location: Nashville, Tenn. Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★★ Financial health: ★★★ Community health survey performance: No survey data Total number of years on 100 Top list: 15 Website

8. Pennsylvania Hospital

Location: Philadelphia Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★ Financial health: ★★ Community health survey performance: No survey data Total number of years on 100 Top list: 2 Website

9. UCHealth University of Colorado Hospital

Location: Aurora, Colo. Clinical outcomes: ★★★★★ Operation efficiency: ★★★★ Patient experience: ★★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 9 Website

10. Penn Presbyterian Medical Center

Location: Philadelphia Clinical outcomes: ★★★★★ Operation efficiency: ★★★★ Patient experience: ★★★★★ Financial health: ★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 5 Website

Top Large Community Hospitals

1. St. David's Medical Center

Location: Austin, Texas Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 14 Website

2. St. David's North Austin Medical Center

Location: Austin, Texas Clinical outcomes: ★★★★★ Operation efficiency: ★★★★ Patient experience: ★★★★ Financial health: ★★★★★ Community health survey performance: No survey data Total number of years on 100 Top list: 5 Website

3. Parkridge Medical Center

Location: Chattanooga, Tenn. Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★ Financial health: ★★★★★ Community health survey performance: 25% Total number of years on 100 Top list: 5 Website

4. Sharp Memorial Hospital

Location: San Diego Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 2 Website

5. Houston Methodist Sugar Land Hospital

Location: Sugar Land, Texas Clinical outcomes: ★★★★★ Operation efficiency: ★★ Patient experience: ★★★★★ Financial health: ★★★★★ Community health survey performance: No survey data Total number of years on 100 Top list: 5 Website

6. Cape Coral Hospital

Location: Cape Coral, Fla. Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★★ Financial health: ★★★★★ Community health survey performance: 100% Total number of years on 100 Top list: 4 Website

7. Saint Mary's Regional Medical Center

Location: Reno Clinical outcomes: ★★★★★ Operation efficiency: ★★★★★ Patient experience: ★★ Financial health: ★★★ Community health survey performance: 100% Total number of years on 100 Top list: 4 Website

8. Medical City Plano

Location: Plano, Texas Clinical outcomes: ★★★★★ Operation efficiency: ★★ Patient experience: ★★★★ Financial health: ★★★★★ Community health survey performance: No survey data Total number of years on 100 Top list: 2 Website

9. Chippenham Hospital

Location: Richmond Clinical outcomes: ★★★★★ Operation efficiency: ★★★★ Patient experience: ★★★ Financial health: ★★★★★ Community health survey performance: 75% Total number of years on 100 Top list: 3 Website

10. Olathe Medical Center

Location: Olathe, Kan. Clinical outcomes: ★★★ Operation efficiency: ★★★★★ Patient experience: ★★★★ Financial health: ★★★★★ Community health survey performance: No survey data Total number of years on 100 Top list: 2 Website

Margin declines, expense growth, and an impending "labordemic" has been spelling trouble for non-profit hospitals looking to claw their way to financial relief.

Median operating and operating EBITDA margins for non-profit hospitals declined significantly from fiscal year 2021 to 2022, Fitch Ratings said, and this decline is primarily due to persistent high labor costs and the inelastic nature of hospital revenue.

In fact, with stimulus funds tapering off, median revenue growth slowed and expenses increased due to a reliance on expensive external contract labor and increased salary and wage costs.

So, what can CFOs of non-profit hospitals and health systems do to fight back?

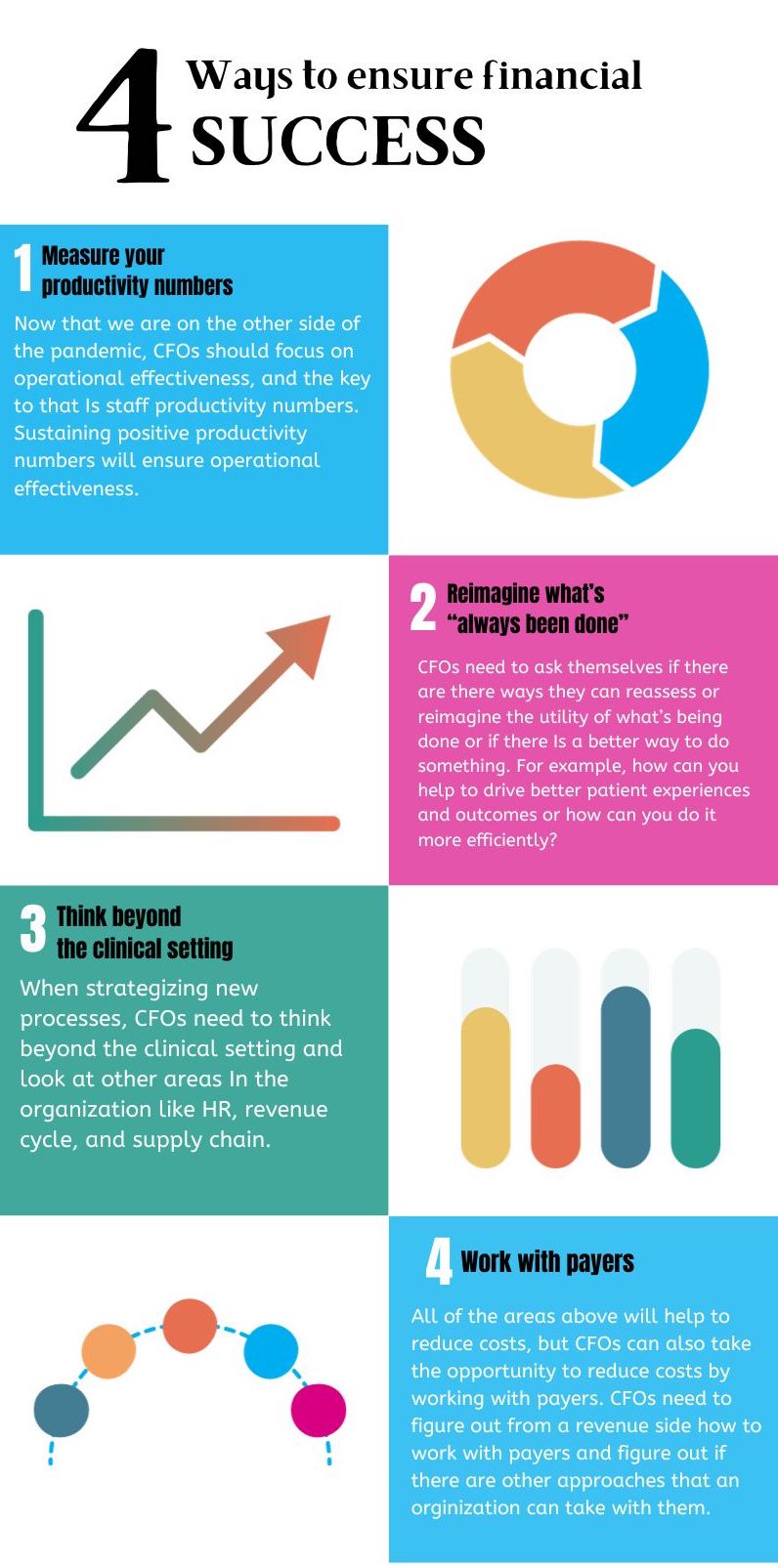

CFOs need to place their focus on operational effectiveness, Brett Tande, CFO of Scripps Health, a $4.3 billion not-for-profit integrated health system in San Diego, California, told me in November.

“Consistent with what we've been showing in our quarterly results throughout 2023, we're probably going to lose about $30 [million] to $40 million in our next earnings report,” Tande says.

“One of the biggest items that we need to focus on is getting back to profitability,” he says.

Why has profitability been a challenge for Scripps? Aside from labor costs and hardships from the pandemic, the system has been undergoing various construction projects even prepandemic. But nonetheless, profitably is what pays for these updates.

“What pays for that is that positive operating cash flow that we need,” he says. “And when it's depressed, you've got to see those debt levels come up. And that's what we've been seeing over the last couple of years. And I think for in 2024, we'll see that more as well.”

That being said, getting that profitability back to a level that can support the organization will be very important, Tande said, “so, I will be working on that.”

The question then becomes, how do you do that?

Tande said the pandemic was very challenging for Scripps, not only financially but obviously for its staff as well.

Now that we are on the other side of the pandemic, Scripps’ focus is on operational effectiveness, and Tande says the last year or two have been really promising.

“Our productivity numbers now look great throughout the organization and we're really just trying to sustain that,” he says. “We think that has a lot of value.”

Aside from maintaining productivity, reimagining what’s “always been done” is necessary as well.

“Are there ways we can reassess or reimagine the utility of what we're doing or is there a better way to do something?” Tande pondered. “How can we help to drive a better patient experience and outcome or how can we do it a little bit more efficiently?”

That's the approach they have to take, he says.

“And again, it's not just in that clinical setting,” Tande says. “Reimagining operations has to be done throughout the organization. It could be in HR, revenue cycle, supply chain, or otherwise, but we need to try to be able to reduce our costs.”

When reducing costs, “there are a lot of irons that we have in the fire across the organization,” Tande says.

And, like most organizations, working with payers isn’t off the table when looking to reduce costs.

“We have to figure out from a revenue side how to work with payers and figure out if there are other approaches that we can take with them,” he says. “Which is something that the entire industry needs to do.”

Staying abreast of the healthcare finance market is a must for CFOs, and there were four stories that were top of mind for leaders.

Here are the four stories that CFOs tracked in 2023:

Mclaren St. Luke's closed down in 2023 due to 'historical financial losses'

McLaren St. Luke’s, a Maumee, Ohio-based healthcare provider, closed the hospital in the spring following years of declining revenues and an unstable reimbursement environment.

"Despite the tireless dedication of everyone associated with McLaren St. Luke’s, we have not been able to overcome the historic financial losses experienced by this hospital—losses that began long before COVID-19 that now run into the millions each month," Jennifer Montgomery, RN, MSA, FACHE, president and CEO of McLaren St. Luke’s, said in a statement announcing the closure. "Our passion for patient care and commitment to clinical excellence have never wavered. But sadly, we are not on a financially sustainable path."

Steward Health Care System CEO said we would see more VBC in 2023

Steward Health Care Systems prides itself on being a leader in the transition to value-based care (VBC). This Dallas-based operator of 39 hospitals across Arizona, Arkansas, Florida, Louisiana, Massachusetts, Ohio, Pennsylvania, Texas, and Utah generates roughly $6.5 billion in annual revenue and was founded on the VBC model.

CEO Ralph de la Torre, MD, connected with HealthLeaders this year to discuss the organization’s success with the VBC model, why hospitals may be reluctant to adopt a VBC model, and why he thought that would change in 2023.

How CFOs are balancing physician compensation with lowering labor costs

Hospital and health system CFOs are facing a bit of a dilemma when it comes to recruiting and retaining physicians. On one end, physician compensation is rising. On the other, slashing labor costs is a priority.

That reality necessitates that CFOs achieve a balancing act between employing top talent while keeping expenses in check. But hospitals' bottom lines aren't just affected by how much it costs to pay a physician. There are also opportunity costs and other expenses associated with physicians walking out the door in search of better compensation.

For that reason, cutting corners with physician salary isn't at the top of CFOs' to-do list. If anything, the opposite seems to be true, with hospitals acknowledging the competitive landscape for attracting and retaining physicians and showing willingness to invest in their workforce.

Deal Or No Deal: 3 ways CFOs can take a stand in contract negotiations with payers

If it seems like contract negotiations between payers and providers are becoming more adversarial and playing out in public more often, that's not just perception—it's the reality in which the fragmented healthcare system currently operates.

Thanks to economic headwinds made up of record inflation and operational challenges, hospital and health system CFOs find themselves with their backs against the wall in negotiations with insurers. Operating margins may be slowly improving, but they remain razor thin for many, especially in comparison to the profits payers continue to reap.

As contracts agreed upon in a different financial climate reach their expiration, the two sides are being forced to come to the table and find new common ground during a new normal in healthcare.

There are significant cultural and operational differences which will need to be accounted for when making moves in 2024.

CFOs will continue to fight against poor operating margins, reduced reimbursement, and inflated expenses in 2024, developing and executing a strategic path to a financially sustainable future is essential. For some, this can mean an acquisition or merger.

Hospitals and health systems of every type are feeling the financial pressure—even nonprofits will continue to grapple with existential questions about their strategy and structure moving forward.

Realizing the fundamental differences between for-profit and nonprofit hospitals will play a large part in a leader’s decision making.

For-profit and nonprofit hospitals are fundamentally similar organizations with subtly different cultural approaches to managing the economics of healthcare. All acute care hospitals serve patients, employ physicians and nurses as their primary personnel, and operate in the same regulatory framework for delivery of clinical services.

There are, however, a few primary differences between for-profit and nonprofit hospitals, which could potentially impact ROI.

TAX STATUS

The most obvious difference between nonprofit and for-profit hospitals is tax status, and it has a major impact financially on hospitals and the communities they serve.

Hospital payment of local and state taxes is a significant benefit for municipal and state governments, said Gary D. Willis, a former for-profit health system CFO said. The taxes that for-profit hospitals pay support "local schools, development of roads, recruitment of business and industry, and other needed services," he said.

The financial burden of paying taxes influences corporate culture—emphasizing cost consciousness and operational discipline. For example, for-profit hospitals generally have to be more cost-efficient because of the financial hurdles they have to clear.

OPERATIONAL DISCIPLINE

With positive financial performance among the primary goals of shareholders and the top executive leadership, operational discipline is one of the distinguishing characteristics of for-profit hospitals, said Neville Zar, the former senior vice president of revenue operations at Steward Health Care System, a for-profit that includes 3,500 physicians and 18 hospital campuses in four states.

When Zar was at the system, a revenue-cycle dashboard report was circulated at Steward every Monday morning at 7 a.m., including point-of-service cash collections, patient coverage eligibility for government programs such as Medicaid, and productivity metrics.

A high level of accountability fuels operational discipline at for-profits, Zar said.

FINANCIAL PRESSURE

Accountability for financial performance flows from the top of for-profit health systems and hospitals, said Dick Escue, former CIO at a health insurance company. Escue also worked for many years at a rehabilitation services organization that for-profit Kindred Healthcare of Louisville, Kentucky, acquired in 2011. "We were a publicly traded company. At a high level, quarterly, our CEO and CFO were going to New York to report to analysts. You never want to go there and disappoint. … You're not going to keep your job as the CEO or CFO of a publicly traded company if you produce results that disappoint."

Finance team members at for-profits must be willing to push themselves to meet performance goals, Zar said.

For-profit hospitals also routinely utilize monetary incentives in the compensation packages of the C-suite leadership, said Brian B. Sanderson, managing principal of healthcare services at Crowe.

"The compensation structures in the for-profits tend to be much more incentive-based than compensation at not-for-profits," he said. "Senior executive compensation is tied to similar elements as found in other for-profit environments, including stock price and margin on operations."

In contrast to offering generous incentives that reward robust financial performance, for-profits do not hesitate to cut costs in lean times, Escue says.

"The rigor around spending, whether it's capital spending, operating spending, or payroll, is more intense at for-profits. The things that got cut when I worked in the back office of a for-profit were overhead. There was constant pressure to reduce overhead," he says. "Contractors and consultants are let go, at least temporarily. Hiring is frozen, with budgeted openings going unfilled. Any other budgeted, but not committed, spending is frozen."

SCALE

The for-profit hospital sector is highly concentrated. In 2023, there are 5,157 community hospitals in the country, according to the American Hospital Association. Nongovernmental not-for-profit hospitals account for the largest number of facilities at 2,978. There are 1,235 for-profit hospitals, and 944 state and local government hospitals.

On the other hand, the country's for-profit hospital trade association, the Federation of American Hospitals, represents 1,000 tax-paying community hospitals and health systems throughout the U.S., accounting for nearly 20% of U.S. hospitals.

Scale generates several operational benefits at for-profit hospitals.

"Scale is critically important," said Julie Soekoro, former CFO of a Community Health Systems (CHS)-owned hospital. And one benefit of being CHS-owned? The access to resources and expertise, Soekoro said at the time.

Best practices are shared and standardized across all CHS hospitals. "Best practices can have a direct impact on value," Soekoro says. "The infrastructure is there. For-profits are well-positioned for the consolidated healthcare market of the future… You can add a lot of individual hospitals without having to add expertise at the corporate office."

The High Reliability and Safety program at CHS is an example of how standardizing best practices across the health system's hospitals has generated significant performance gains, she says.

Scale also plays a crucial role in one of the most significant advantages of for-profit hospitals relative to their nonprofit counterparts: access to capital.

Ready access to capital gives for-profits the ability to move faster than their nonprofit counterparts, Sanderson says. "They're finding that their access to capital is a linchpin for them. … When a for-profit has better access to capital, it can make decisions rapidly and make investments rapidly. Many not-for-profits don't have that luxury."

COMPETITIVE EDGE

There are valuable lessons for nonprofits to draw from the for-profit business model as the healthcare industry shifts from volume to value.

When healthcare providers negotiate managed care contracts, for-profits have a bargaining advantage over nonprofits, Doran says. "In managed care contracts, for profits look for leverage and nonprofits look for partnership opportunities. The appetite for aggressive negotiations is much more palatable among for-profits."

This article was adapted from previous coverage. Reread it here.

Editor's note: This story was updated on 12/29/2023.

"The growth in healthcare spending in 2022 of 4.1% was more consistent with the pre-pandemic average annual growth rate of 4.4% over 2016-19," Micah Hartman, a statistician in the CMS Office of the Actuary and first author of the report, said in a media release.

"It remains to be seen how future healthcare spending trends will materialize, as trends are expected to be driven more by health-specific factors such as medical-specific price inflation, the utilization and intensity of medical care, and the demographic impacts associated with the continuing enrollment of the baby boomers in Medicare," Hartman said.

Below are a few more key takeaways from the report, and you can read John Commins full report here.

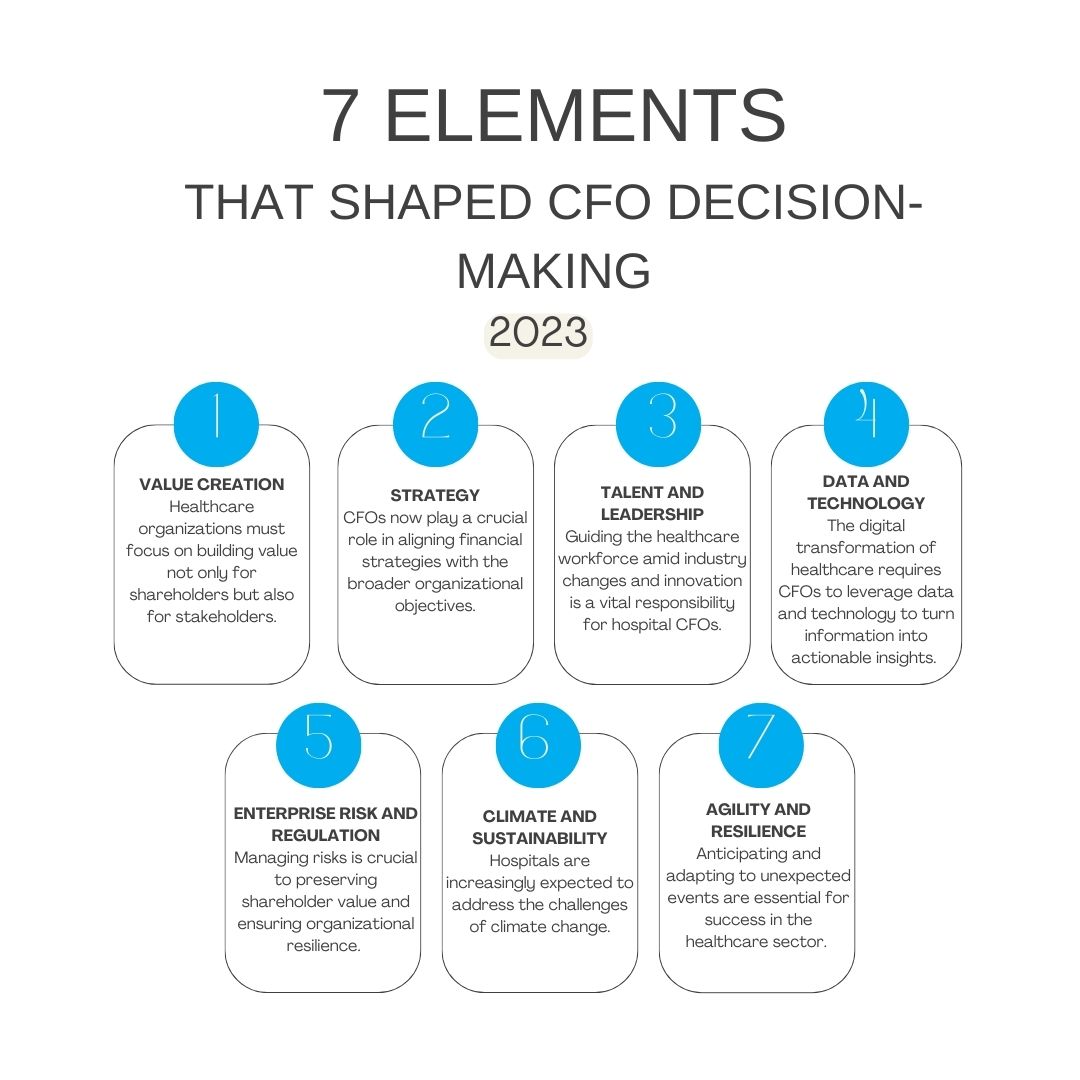

There were seven main threads propelling CFOs' decision making in 2023.

CFOs now find themselves at the intersection of various critical drivers that shape the financial outlook and strategic direction of their healthcare organizations.

So, what were the main threads propelling their decision making in 2023?

There were seven elements that encapsulated the key considerations for CFOs across all industries in 2023, according to Deloitte. Take a look at these seven drivers and read our full story to learn how each applied to CFOs in the healthcare sector.

A new bill may cause a shake-up for hospital and health systems.

The Lower Costs, More Transparency Act, a bipartisan healthcare policy bill, recently passed the House of Representatives, setting the stage for a potential shake-up for healthcare organizations.

This legislation aims to increase hospital price transparency and curb certain practices by pharmacy benefit managers (PBMs).

But why is it significant?

Well, of particular significance is the proposal to equalize payments for drugs in Medicare, whether or not they are administered in hospital outpatient departments or doctor's offices.

Additionally, the bill seeks to postpone payment cuts for hospitals catering to high volumes of uninsured patients until 2026, a delay from the previously anticipated 2023.

Healthcare organizations also need to be on the lookout for increased price transparency scrutiny, especially as many organizations are still struggling with adherence.

What does it mean for CFOs?

Crucial for hospital and health system CFOs is the potential impact of the bill's site-neutral policy on drug reimbursements in Medicare.

Hospitals' opposition to the equalization of drug payments, contending that it would cut into hospital revenue, underscores the financial implications for healthcare institutions

With the legislation projected to reduce hospital payments by over $3.7 billion over a decade, CFOs must carefully navigate the financial landscape amid evolving policies.

The bill also introduces transparency reforms for PBMs, addressing issues of spread pricing and mandating the disclosure of rebates and compensation. This legislative push aligns with broader efforts to scrutinize and regulate PBMs, acknowledging their role in influencing rising drug prices.

For CFOs, adapting strategies to comply with potential transparency requirements and understanding the financial implications of proposed changes will be pivotal.

3474.jpg)